When Should I Claim Social Security?

On January 31, 1940, Ida May Fuller of Ludlow, Vermont, was the first person to receive a Social Security check. That historic payment amounted to $22.54. Before retiring in November 1939, she served as a legal secretary and contributed to Social Security for about 2½ years. Total taxes paid: $24.75. Before passing away in 1975, she had collected $22,888.92 in benefits.

Today, more than 73 million people receive some type of Social Security benefit, including supplemental income and disability benefits. Nearly 55 million people are receiving retirement benefits, according to the Social Security Administration, with an average monthly benefit of $1,931 (Retired workers: $1981; spouses of retired workers: $932). Most folks are eligible for Social Security. How much you are entitled to receive depends on your highest 35 years of indexed earnings and the age you apply for benefits.

While there are legitimate concerns about the long-term funding viability of Social Security, we also need to be careful about over-speculating on future tax and political agendas. While some adjustments to the program will be needed, it’s not likely to go away any time soon, and will continue being an integral part of most American’s retirement plans. For folks facing these decisions now, or in the next few years, it should be based on what we know today. For those with a longer timeline until retirement, changes won’t be made overnight, giving us a runway to adjust your plan.

Table 1 highlights when you are eligible to receive full Social Security benefits. For example, if you were born in 1958, you are eligible to receive your full benefit at age 66 and 8 months.

Under current law, the full retirement age no longer rises for those born after 1960.

File today or delay?

You can begin collecting benefits when you turn 62 years old. But is that a wise decision?

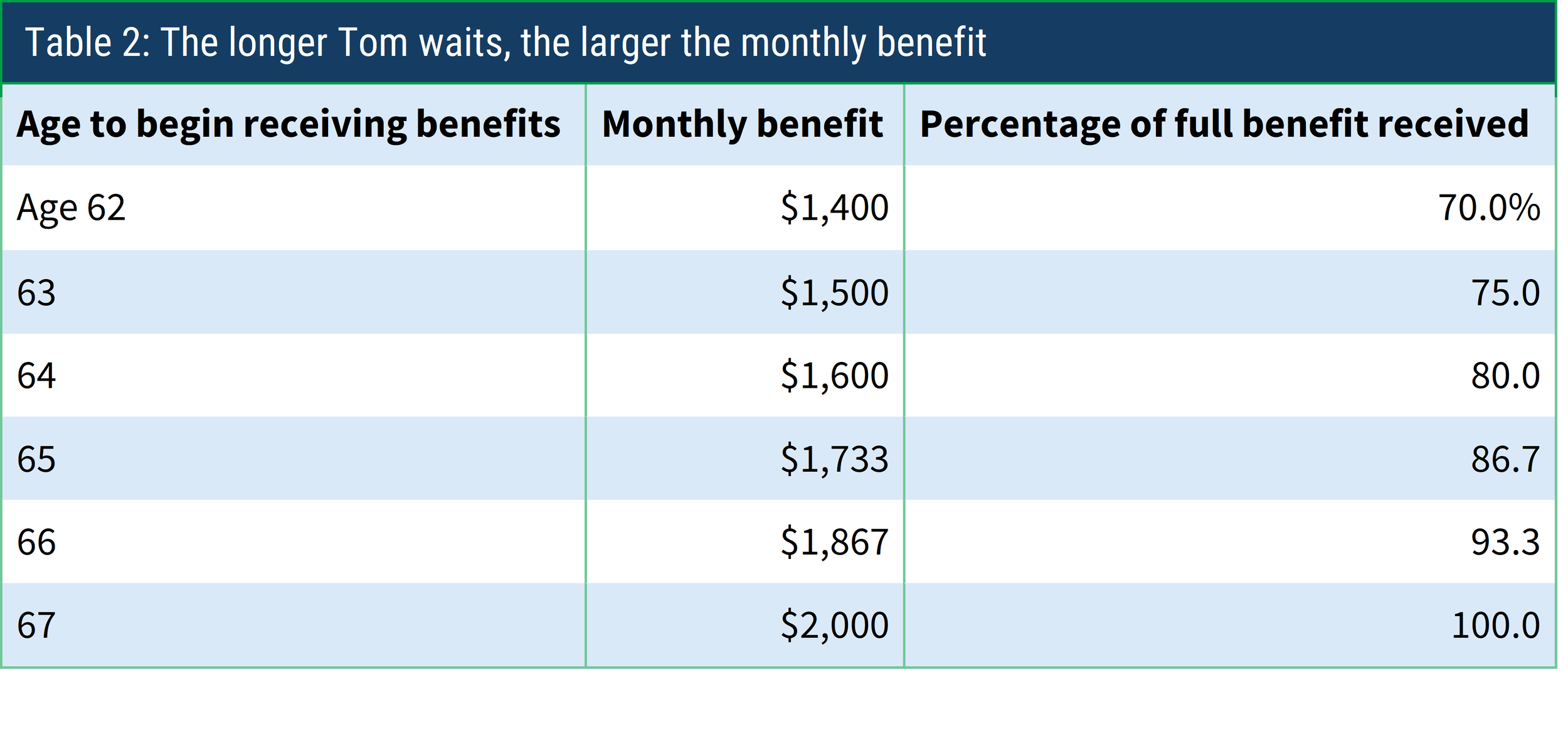

Tom was born in 1963, and he just turned 62. He is eligible for Social Security. If Tom waits until 67, he will receive a monthly payment of $2,000 based on his income. If, however, he files for benefits at 62, his monthly check would be 70% of the full benefit or $1,400 per month.

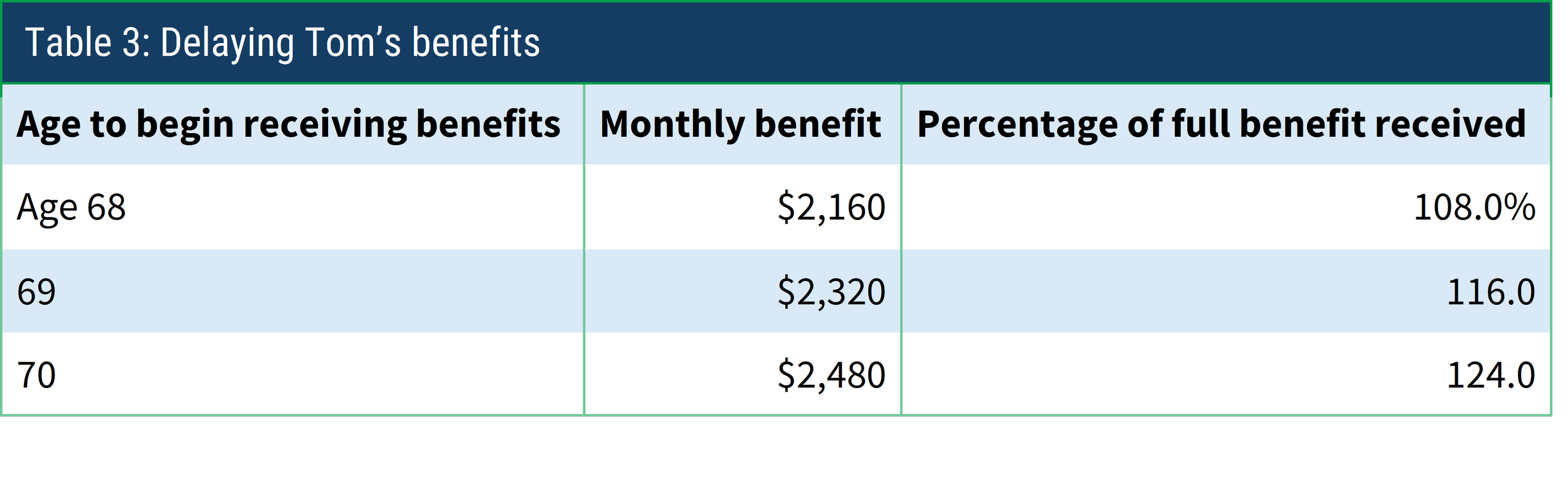

Continuing with our original example, can Tom delay benefits past 67? Yes, and he’ll be entitled to a larger monthly check (Table 3).

Tom may also file at any time during the year, and his monthly check will be prorated (in twelfths). Note that the 8% increase each year is based on the original FRA benefit of $2,000, which is referred to as simple interest, instead of compounding interest.

You will not accrue additional benefits beyond your 70th birthday. Unless there is a compelling reason to delay benefits, it’s best to begin collecting when you turn 70.

A bird in the hand or two in the bush?

“I’m eligible for monthly benefits. Should I file today or delay?”

Filing for Social Security at 62 will result in a permanently lower monthly benefit over a longer period. Wait until 70, and you maximize your monthly payment, but you’ll receive fewer checks. Also, if you are working and under full retirement age, your benefit may be reduced.

Many variables can be inputted into the calculation. There is no magic formula. It’s a personal decision and can be complex. Conventional wisdom suggests that if you don’t need the money today, consider delaying as long as you can. But it’s not always that simple.

Basic guidelines

What are your cash needs? Are you still working? If you are, does your monthly income meet or exceed your expenses? If so, it may be wise to delay.

If you have retired, could you consider working part-time? However, if you have fewer resources and can’t work, your options may be limited.

Additionally, there are considerations regarding life expectancy and health. When a male turns 67, Social Security estimates life expectancy at 82.63 years. For a female, that rises to 85.23 years.

Claim early

You simply want to retire, and Social Security, combined with savings, enables you to do so.

Are you in poor health, or are you battling a chronic health condition? If so, it may be advantageous to claim early.

Has the stock market suffered a prolonged downturn? Claiming early could lighten the income burden from your investment portfolio, allowing it to recover more quickly.

The breakeven is roughly between 78 and 82 years old but can vary based on factors such as cost-of-living adjustments.

Claim later

You enjoy working. That’s what gets you up in the morning. Sure, the income is a motivator, but you don’t dread Monday mornings.

The future is unknown, but you are in good health, and your family history suggests a longer life expectancy.

You have other sources of income, such as rental properties, a pension, consulting income, or a part-time gig. Put another way, you wouldn’t mind the extra cash from Social Security, but it’s not needed.

The bridge between retirement and 70

What if you retire before age 70 but want to wait until age 70 to apply for benefits?

You have savings, but your cash inflow has been reduced. Your bills are a priority, and a reduced cash inflow must be made up somewhere.

Making larger withdrawals from your retirement portfolio is an option, but it will result in a smaller nest egg to appreciate as you age.

So, how can you bridge the gap? Is your spouse still working? Can you reduce expenses? Do you have a pension that can help cover the gap between retirement and age 70?

These are just some of the factors that come into play.

What about your spouse?

Your spouse may claim benefits based on a husband’s or wife’s earnings as long the person is 62 or older, and the person’s spouse is already receiving a monthly Social Security check.

Your full spouse’s benefit could be up to one-half the amount your spouse is eligible to receive at their full retirement age. If you receive your spouse’s benefits before you reach full retirement age, your payment will be permanently reduced.

However, your maximum spouse’s benefit remains 50% of the full retirement age benefit, not their higher amount, including delayed retirement credits. For example, if the higher earner's full retirement age benefit is $2,000, the spousal benefit is capped at $1,000 (50%). If the higher earner waits to 70 and their benefit increases to $2,400, the spousal benefit remains at $1,000.

Yet, if you need Social Security sooner, the lower-earning spouse can file based on their income, which allows the higher-earning spouse to delay. When the higher earner begins to collect, the lower earner is eligible to switch to a higher spousal benefit, assuming, of course, the spousal benefit is higher.

Summary

Your decision should not be made in a vacuum. Social Security guidance should be part of any well-constructed comprehensive plan. It should incorporate many factors such as fixed income needs, other income sources, health and life expectancy, tax planning, and market conditions.

That said, we don’t expect you to make this decision alone. As a fee-only fiduciary planner, we can provide unbiased advice to make sure you get it right. We understand the complexities involved, and we can help you evaluate various scenarios tailored to your circumstances. Ultimately, the decision is yours. It’s personal, but we would be happy to assist you if you have any questions.

*Facts in this article sourced from SSA.gov